Estratégias eficazes para controlar seu orçamento familiar

Descubra conteúdos exclusivos que simplificam o gerenciamento financeiro, ajudando você a tomar decisões inteligentes e seguras para seu futuro econômico.

Dicas práticas para aprimorar seu controle financeiro

This section provides a detailed and comprehensive overview of your company’s mission, values, and history. It highlights the key principles and values that drive the purpose, goals, and long-term success of your brand and business operations.

Finanças Pessoais

Descubra artigos detalhados sobre finanças pessoais, incluindo dicas de orçamento, orientação sobre empréstimos estudantis e seguros para ajudar você a controlar seu dinheiro com confiança.

-

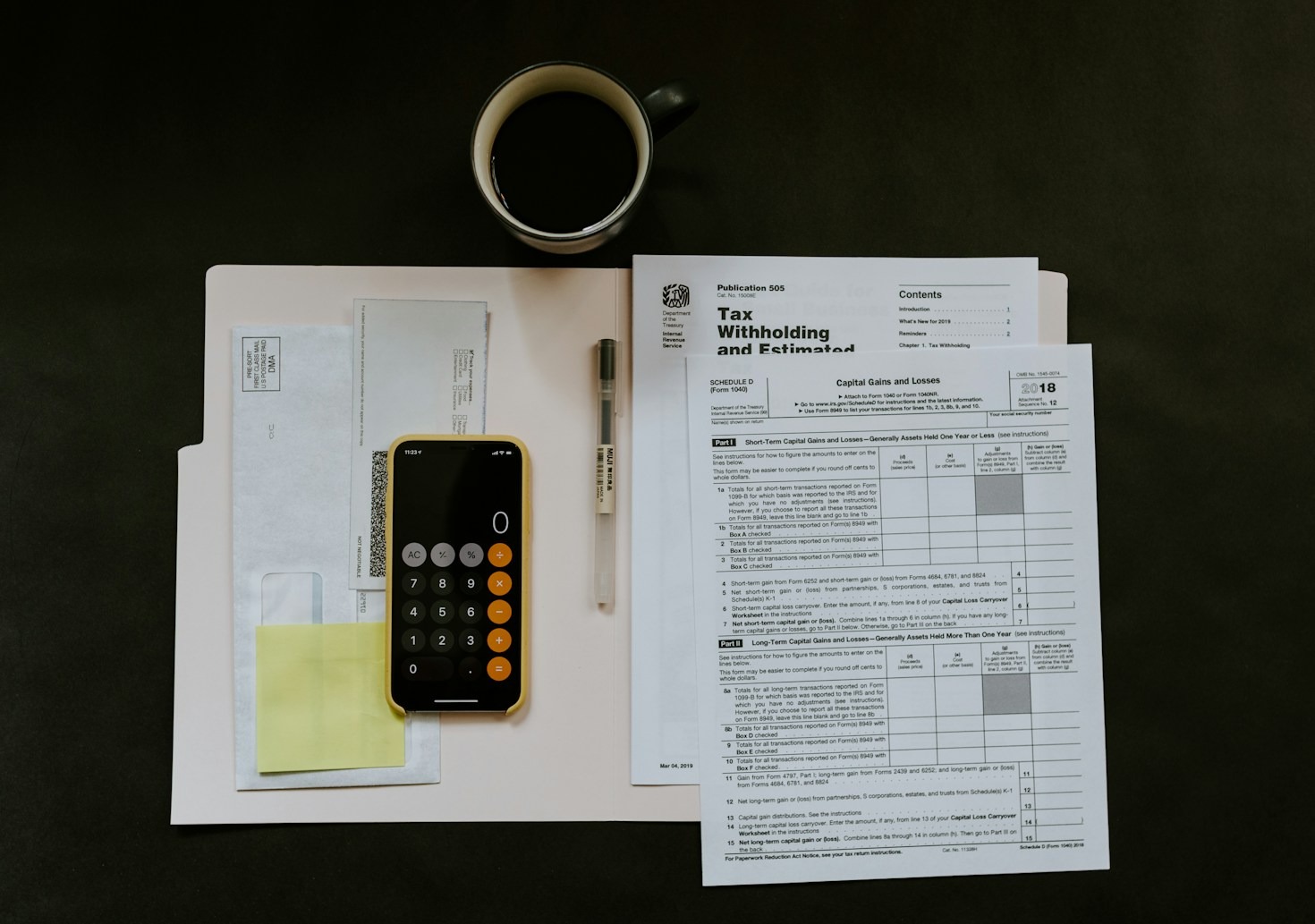

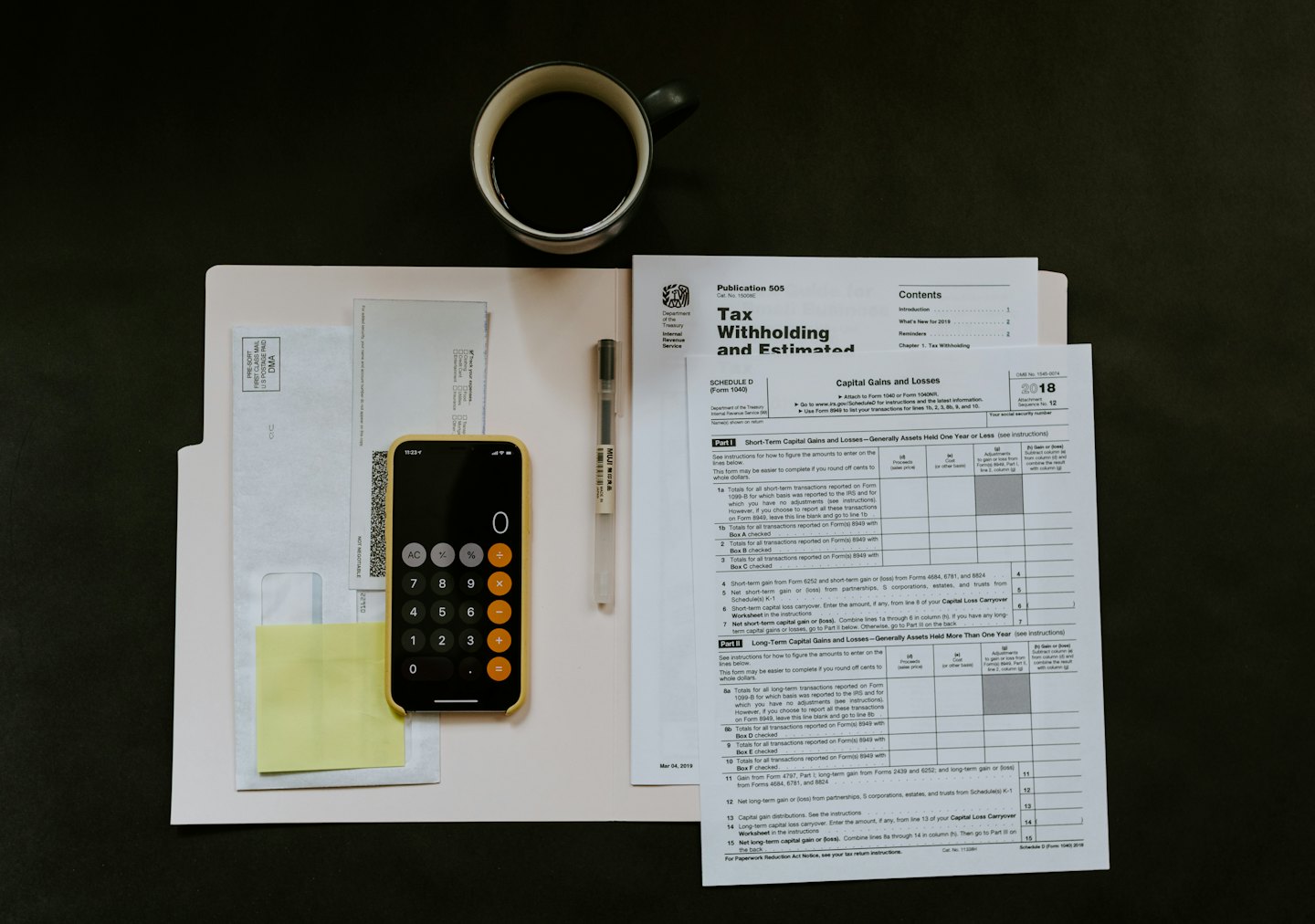

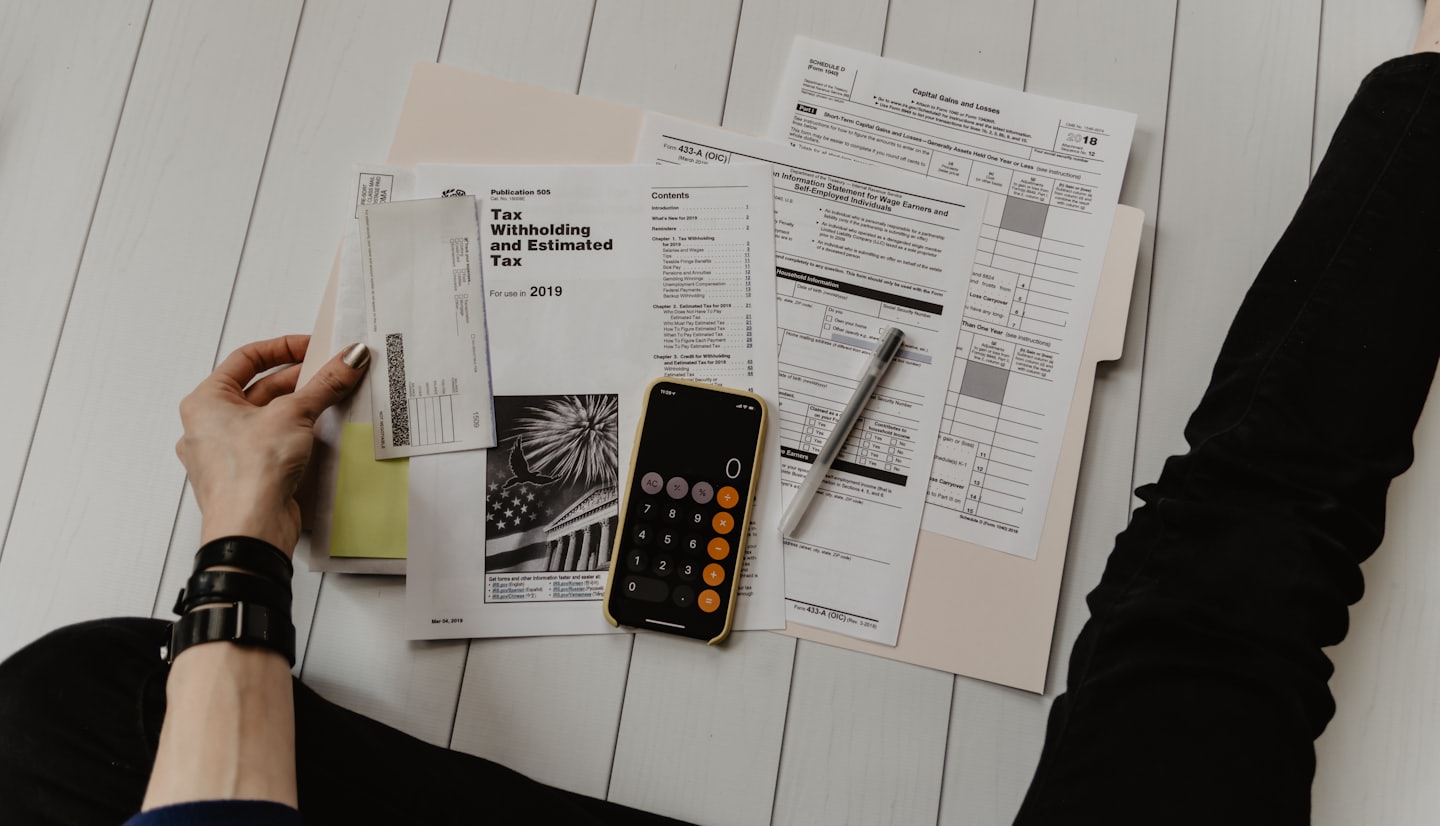

Como Organizar o Orçamento Familiar e Melhorar Suas Finanças

Manter o controle do orçamento familiar é essencial para garantir uma vida financeira equilibrada. Muitas famílias enfrentam dificuldades para administrar seus recursos, principalmente quando não existe um planejamento claro sobre como o…

-

Estratégias Eficazes para Controlar Seu Orçamento Familiar

Controlar o orçamento familiar é uma das práticas mais importantes para garantir estabilidade financeira e evitar problemas com dívidas. Muitas famílias enfrentam dificuldades financeiras não necessariamente por falta de renda, mas pela…

-

Gestão de dinheiro: hábitos que transformam sua vida financeira

Este parágrafo serve como uma introdução ao seu post no blog. Comece discutindo o tema principal ou o tópico que você planeja abordar, garantindo que ele capte o interesse do leitor desde…

Domine suas finanças com dicas práticas e confiáveis

Descubra conteúdos essenciais que ajudam você a gerenciar dinheiro, empréstimos e seguros com clareza.

Finanças Pessoais

Aprenda os fundamentos para controlar seu orçamento e reduzir dívidas.

Planejamento Financeiro

Conheça métodos eficazes para organizar suas finanças a longo prazo.

Dicas Práticas

Encontre orientações valiosas para poupar e investir com confiança.

Dicas práticas para gerir suas finanças pessoais

Aqui você encontra dados relevantes, com análises sobre indicadores financeiros essenciais e resultados alcançados.

130

Empréstimos Estudantis

Informações detalhadas sobre como gerenciar e quitar seus empréstimos estudantis com eficiência.

210

Orçamento Pessoal

Sugestões valiosas para equilibrar suas receitas e despesas de forma sustentável.

320

Seguros Essenciais

Orientações sobre as principais apólices para proteger sua saúde, vida e patrimônio.

410

Planejamento Financeiro

Conselhos práticos para organizar seus recursos e alcançar estabilidade financeira.

Guia Essencial para Suas Finanças Pessoais

Descubra dicas práticas e informações detalhadas para ajudar você a controlar seus empréstimos estudantis, seguros e orçamento com confiança.